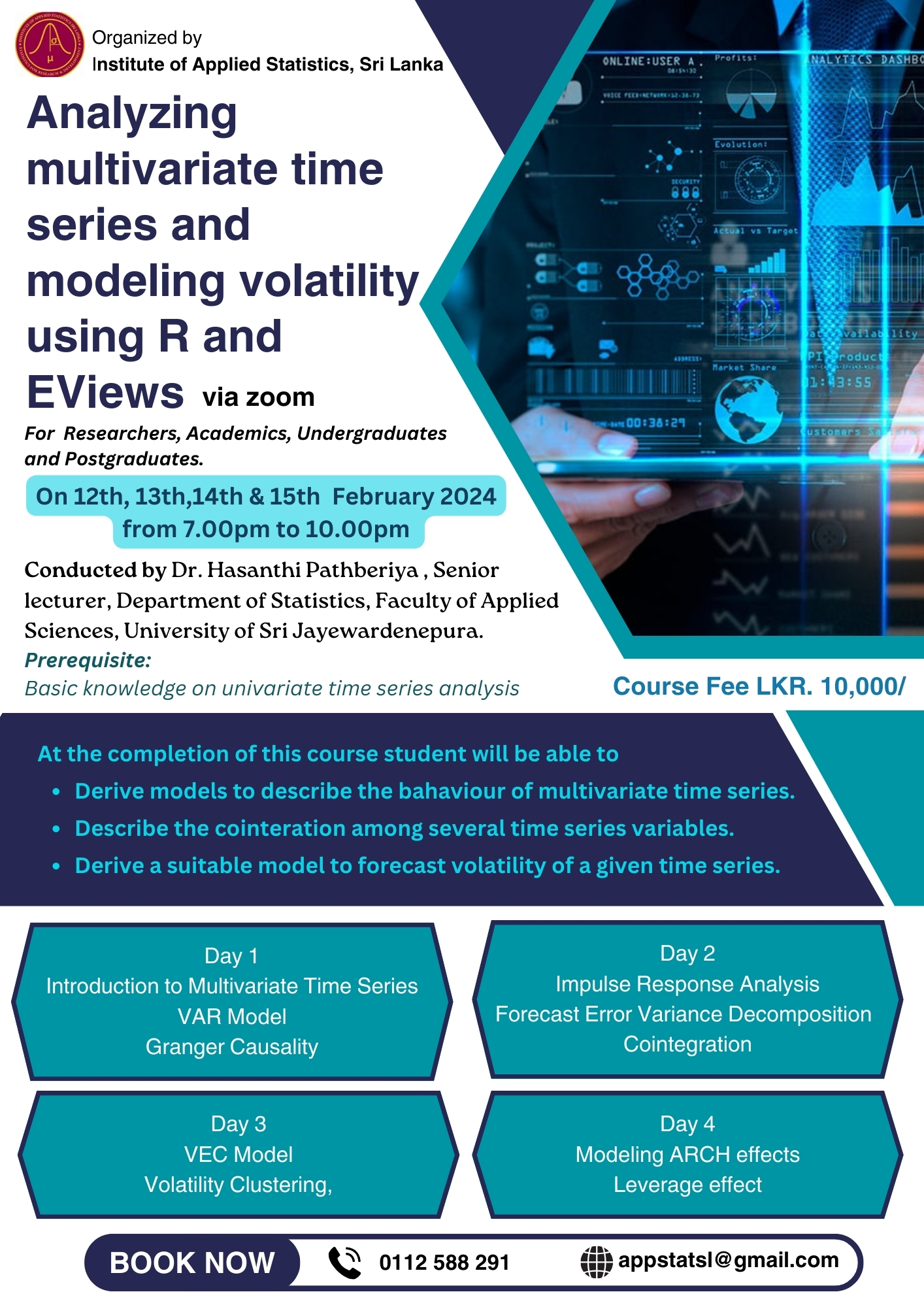

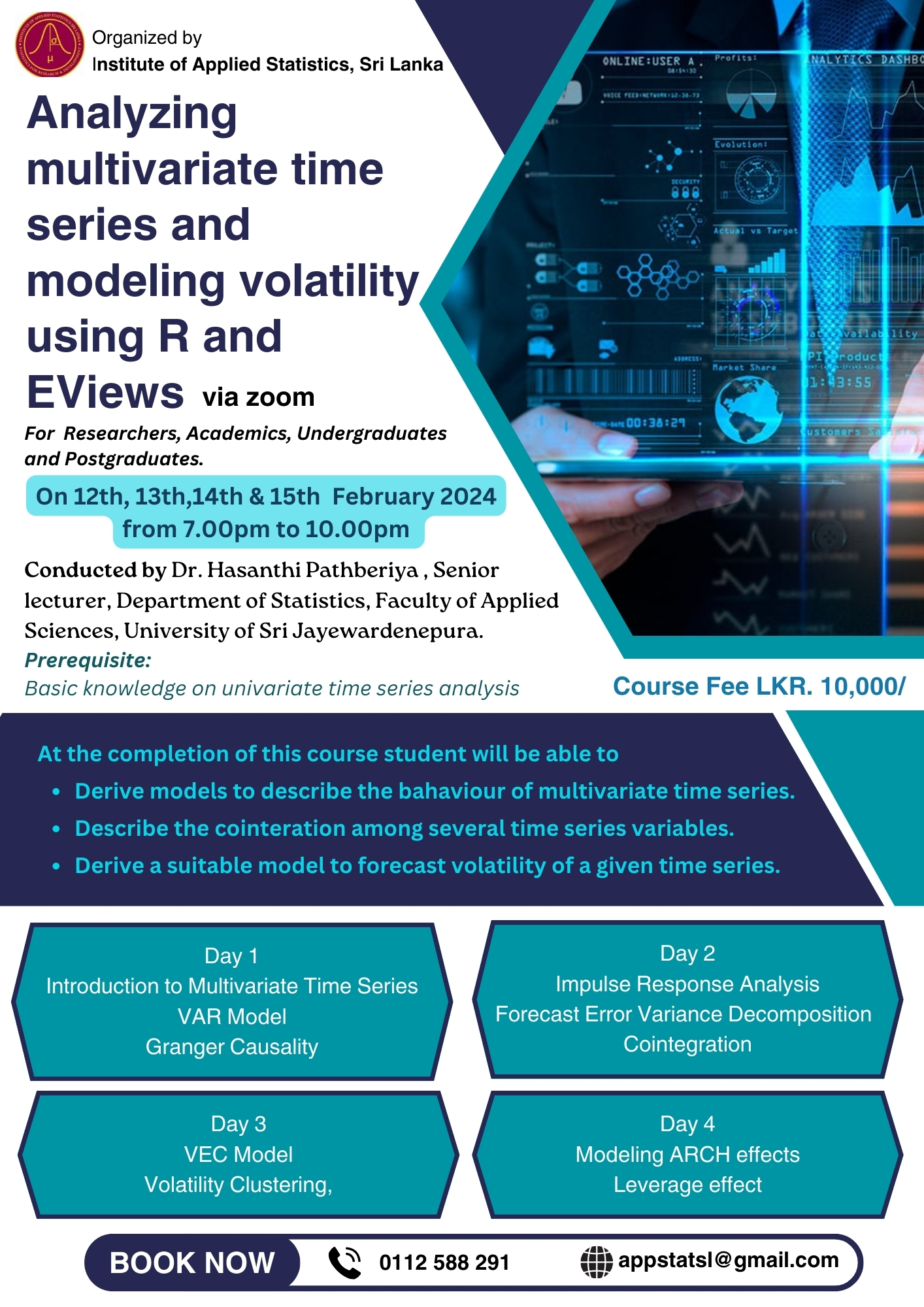

Analyzing multivariate time series and modeling volatility using R and EViews

Learning Outcomes: At the completion of this course students will be able to

* Derive models to describe the behavior of multivariate time series.

*Describe the cointegration among several time series variables.

*Derive a suitable model to forecast the volatility of a given time series.

Analyzing multivariate time series and modeling volatility using R and EViews.

Resource Person: Dr. Hasanthi Pathberiya. Senior Lecturer. Dep. of Statistics, Faculty of Applied Sciences, University of Sri Jayewardenepura, Sri Lanka.

Course Fee: LKR. 10,000/

Account No: 086100130008638

Account Name: Institute of Applied Statistics Sri Lanka

Bank: People's Bank, Thimbirigasyaya.

(Payment should be made on or before 9th February 2024)

features